Borrowers will benefit from greater transparency on personal loans online thanks to a major change to the Consumer Data Right. Clearer comparison and application procedures are made possible by the reform, which mandates that non-bank lenders share consumer data with major banks.

Significant modifications to the Consumer Data Right framework that expand data-sharing responsibilities to non-bank lenders were announced by the Australian government on March 4, 2025. Consumers will be able to compare rates, fees, and suitability when applying for credit thanks to safe access to their personal financial data starting in July 2026. With $9.3 billion borrowed in fixed-term consumer loan in the September quarter of 2025, the expansion is expected to change the way that large banks and specialised online lenders like CashPal evaluate candidates and present offers.

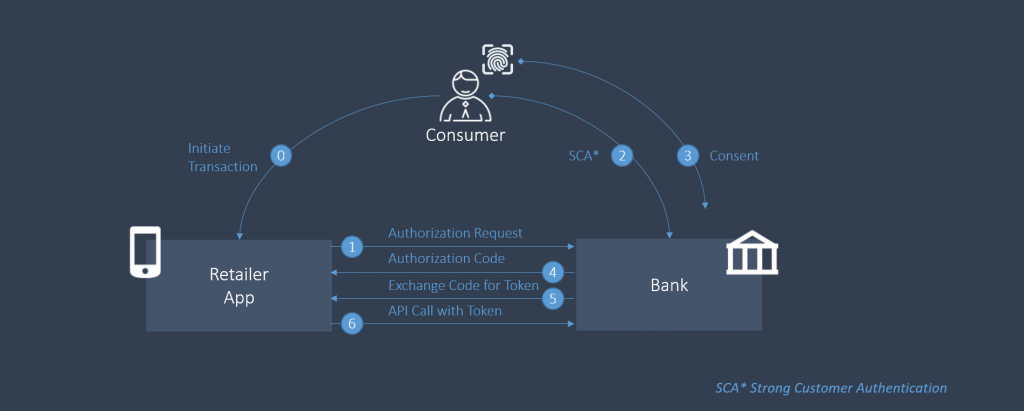

Understanding the Consumer Data Right Framework

The Consumer Data Right represents a fundamental shift in financial data ownership. Currently, when Australians apply for personal loans online, they manually gather payslips and bank statements. Applicants often submit identical information to multiple lenders hoping to secure competitive rates. The process is time-consuming and creates friction in the borrowing experience.

The CDR changes this dynamic entirely. Consumers will grant secure permission for their banking institutions to share verified data directly with accredited lenders or comparison services. This eliminates redundant documentation and allows actual banking history to demonstrate financial capacity.

Australia has been implementing CDR since 2020, beginning with major banks. The system has already processed more than 4 billion consumer data requests. The expansion to non-bank lenders represents the next phase of this economy-wide reform, bringing transparency to a broader segment of the personal lending market.

The framework operates on consent-based principles. Consumers control which entities access their data and the duration of access. They retain the right to revoke permissions at any time. This structure differs fundamentally from screen scraping practices where some comparison services previously requested banking credentials. CDR uses secure channels with regulatory oversight from the Australian Competition and Consumer Commission and the Office of the Australian Information Commissioner.

Implementation Timeline for Non-Bank Lenders

The rollout follows a staged approach across 18 months:

- Phase One: 13 July 2026

Product data sharing commences for initial providers. Non-bank lenders with loan portfolios exceeding $10 billion must share standardised product information. This data becomes publicly available in machine-readable format. - Phase Two: 9 November 2026

Consumer data sharing begins for initial providers. The largest non-bank lenders start sharing actual consumer data with appropriate permissions. - Phase Three: 10 May 2027

Additional non-bank lenders meeting specific threshold criteria join the framework. - Phase Four: 13 September 2027

Full implementation across the non-bank lending sector creates a level playing field where traditional banks and alternative lenders operate under consistent data-sharing standards.

These dates apply to non-bank lenders including established names in the digital lending space. Providers such as Plenti, Wisr, MoneyMe, Latitude, and CashPal will progressively integrate CDR capabilities depending on their loan portfolio size.

Key Changes in Lending Transparency

Three significant developments will reshape the personal loan comparison landscape.

Personalised Rate Assessment

Advertised rates of “from 6.17% p.a.” often mislead consumers. Most borrowers don’t qualify for headline rates, which typically apply only to applicants with exceptional credit profiles above 800. Lenders assess individual risk factors, and actual approved rates frequently differ substantially from marketing materials.

CDR enables lenders to evaluate genuine financial positions instantly. Consumers receive tailored rate quotes without submitting formal applications. This process uses soft credit inquiries that don’t impact credit scores. Applicants gain clarity within minutes regarding realistic rate expectations based on their actual circumstances.

Traditional multi-lender applications generate multiple credit inquiries that temporarily reduce credit scores. CDR eliminates this concern by allowing consumers to share verified banking data once.

Comprehensive Fee Disclosure

Fee structures significantly impact total borrowing costs. A $200 establishment fee represents 4% of a $5,000 loan. Comparing fees across lenders traditionally required reviewing multiple product disclosure statements.

CDR mandates standardised product reference data presentation. All fees must be disclosed upfront in machine-readable formats. This standardisation enables direct comparison of establishment fees, monthly account keeping charges, and early repayment penalties.

Accelerated Approval Processes

Manual document verification creates processing delays that often span several days or weeks. CDR streamlines verification by transferring verified banking data securely in real time. Lenders confirm income and expenditure patterns instantly. This reduces approval timeframes substantially.

Reduced error rates benefit both consumers and lenders. Manual data entry introduces mistakes that CDR eliminates by sourcing information directly from verified banking records.

Practical Implications for Borrowers

- Improved Loan Matching – Lenders gain visibility into actual income patterns and spending behaviours. Self-employed applicants with irregular income can demonstrate true earning capacity more effectively.

- Reduced Processing Time – Applications requiring three to five days under current processes could complete within hours. Single-permission data sharing eliminates repetitive document uploads.

- Cost Savings Through Competition – Enhanced transparency intensifies competitive pressure. A 0.5% interest rate reduction on a $20,000 loan over five years generates savings exceeding $500.

- Enhanced Data Security – Consumers maintain control over data sharing parameters and consent durations. This approach offers substantially greater security than sharing banking passwords.

- Streamlined Debt Consolidation – With 52% of Australian personal loans used for debt consolidation according to industry data, lenders can now assess existing debt structures and create appropriate offers.

Buy Now, Pay Later Integration

The CDR expansion incorporates Buy Now Pay Later services. Providers including Afterpay and Zip face new data-sharing obligations under the revised framework.

This integration addresses a significant gap. BNPL usage affects borrowing capacity, yet these services historically haven’t appeared on credit reports like traditional credit products. Under CDR, lenders accessing consumer data will see BNPL commitments alongside other financial obligations.

For responsible BNPL users, this creates a more comprehensive picture of financial management capabilities. The outcome should be more prudent lending practices and reduced instances of consumers accumulating unmanageable debt levels.

Preparation StrategiesCurrent Actions

- Check credit scores through free services including Equifax, Experian, or illion

- Review banking transaction histories to ensure accounts demonstrate consistent financial management

- Consolidate financial information and identify primary income accounts

- Determine which accounts should be included in CDR data-sharing authorisations

Industry data indicates average personal loan borrowers maintain credit scores of 782. Scores below 700 warrant improvement efforts before mid-2026 implementation.

Post-Implementation Steps

When systems activate in July 2026, investigate CDR-enabled comparison services. Verify CDR accreditation through the official register at cdr.gov.au. Begin with a single trusted service to understand the data-sharing process.

Key Reference Points:

- Official CDR Information: cdr.gov.au

- Credit Score Services: Equifax, Experian, illion

- Consumer Protection: ACCC, OAIC

- Financial Counselling: National Debt Helpline 1800 007 007

Only authorise accredited data recipients. Legitimate CDR services never request banking passwords. The framework operates through secure channels exclusively.

Market Context and Future Outlook

The Australian personal loan market reached record volumes in 2025. Market analysis projects continued growth with the sector valued at AUD 2.04 billion in 2025 and forecast to expand at 23% compound annual growth through 2035.

FinTech Australia projects 5.4 million Australians will actively use CDR-enabled services by 2030. This represents approximately one in four eligible consumers.

For lenders across the spectrum, from traditional institutions to digital-first providers like CashPal, CDR compliance creates both obligations and opportunities. Providers must invest in technical infrastructure and data management systems. In return, they gain access to verified consumer data that enables better credit decisions.

Australian borrowers seeking personal loans online will experience a fundamentally different landscape from July 2026. Increased transparency and enhanced comparison capabilities represent significant improvements over current manual procedures. The regulatory framework aims to balance innovation with consumer protection, creating an environment where competition benefits borrowers through better rates and more accessible credit options.